Justin Marleau, the Vice-President of AGSEM, McGill’s teaching union, provided a critical appraisal of the University’s finances at March 22 presentation for Labour Week at McGill.

This analysis comes as University administrators across the province prepare to implement provincial budget cuts. At McGill, the cuts have taken a toll on staff, as the University asks different campus groups to accept wage and hiring freezes for the upcoming year and warns of layoffs.

In an interview with The Daily, Marleau explained that the McGill University Non-Academic Certified Association (MUNACA) strike last semester, and the student movement of the past year, prompted him to look into the University’s finances.

“[I was] trying to figure out why McGill was always running deficits every single year. Because it is highly unusual that an organization would continuously run deficits every single year, unless there is something systematically wrong.”

One of Marleau’s problems with the University’s financial reporting practices is the significant gap between its projected and actual expenses and revenues. For example, operating revenues were projected to be $602.7 million in 2011 fiscal year (FY) and $652.7 million in the FY 2012 budget. The actual operating revenues, however, were $630.9 million in FY 2011 and $709.8 million in FY 2012.

Vice-Principal (Administration and Finance) Michael Di Grappa told The Daily in an email that the inconsistency came in 2011 from changes to the measurement of the fiscal year, following a government mandate to change the end of the year from May 31 to April 30.

“FY 2011 was an 11 month reporting period. The difference is therefore based on real tuition not being prorated over the 11 month period while the budget had prorated tuition and fees for 11 months.”

Di Grappa attributed the discrepancy in 2012 “to sales of goods and services due to the operations of an additional residence (Carrefour Sherbrooke) and government grant adjustment, mostly related to enrolment.”

According to Marleau, some of the differences between budget projections and actual financial statements occur “because the assumptions behind the budgets turn out to be wrong.” To illustrate this, Marleau showed the enrolment projections included in the FY 2008 budget. At the time, the University calculated enrolment increases of no more than 2 per cent a year and decreases in almost every year of Doctoral enrolment. The actual enrolment of all full-time students, however, shows a different landscape, with increases of over 3 per cent for most years, including a 7.2 per cent increase for a year in which a decrease was projected.

According to Marleau, “there is no real explanation to be given, they just make assumptions, and for the enrolment data it is very surprising because you control it.”

Di Grappa told The Daily: “We have no control over how many students will accept the offers in any one year. Our past experience is that we have had more acceptances than anticipated,” he continued.

After this, Marleau focused his talk on the operating deficits the University has been running since 2007, and the decisions that cause these deficits.

McGill’s finances are divided into four funds: the operating fund, dealing with day-to-day expenses; the restricted fund; the Plant Fund, encompassing the capital assets of the University; and the endowment fund, essentially the University’s investment portfolio.

Marleau stated that operating deficits, as defined by McGill, occur only after inter-fund transfers. “One should look at [the period] before the transfers to see if the operations are running the deficits or if it truly is caused by other activities.”

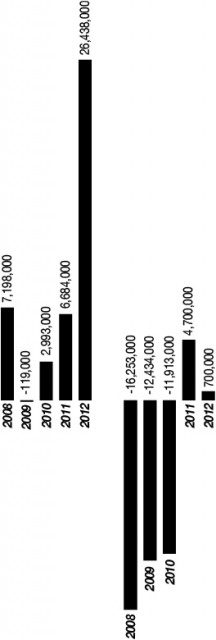

According to Marleau’s calculations, for example, in FY 2008, the University had an operating surplus of $7,198,000 before inter-fund transfer, and a $16,253,000 deficit after the transfer. This is the biggest discrepancy in the period between 2008 and 2012, but all years show a drop in the operating fund.

In the presentation, Marleau stated that the money transferred is going to capital purchases and to cover shortfalls created when payouts from the University’s endowment were reduced from 5 per cent to 4.25 per cent in 2010.

However, Marleau also pointed to the growth in expenses within the Operating Fund since FY 2007. 18 per cent was in academic salaries, which did not grow after 2010; 9.2 per cent in student salaries, 30.2 per cent in administrative and support staff; 39.1 percent in benefits, largely due to changes in benefits calculations, and 535 per cent in student aid, though he noted this growth only represents $22.7 million.

Within the administrative and support staff growth, Marleau also highlighted that the increase can be largely attributed to a 33 per cent increase in management positions from 2006 to 2011.

Speaking to this, Marleau suggested a reorganization of McGill’s managers, stating that the “increase in centralized administrative managers is troubling, as it is not clear why the growth is so large.”

Marleau later spoke to how choices could be made differently to avoid the current cuts McGill has to undertake.

“Maybe we should target those expenses that have raised too high a rate, rather than expenses that have not. That’s why I wanted to look at those specific items and then see where’s the money going, because you can’t, if you spend the money in a targeted manner and then force across the board cuts, you’re not doing it correctly,” Marleau told The Daily.

As such, Marleau has called for the re-evaluation of capital assets and needs. “The infrastructure is the problem, not the cost of employees, so from my perspective the operating fund normally would be fine if the infrastructure wasn’t problematic.”

In the presentation, he pointed to the $822 million in deferred maintenance costs for capital assets that are themselves only worth $1.2 billion.

When asked by The Daily if these costs could be reduced, Di Grappa stated: “The $822 million is the current value of work required to bring the buildings back to an acceptable state of operations. The $1.2 billion represents the cost of acquisitions of all our current capital assets. The two don’t relate.”

Marleau later pointed to potential discrepancies in the numbers and uncertain questions for the future.

“The evaluation of the capital infrastructure was done at the height of the corruption scandal here in Montreal for public works,” he said, “but to be quite honest, it may not actually be that high.”

“Should we try to have different buildings? Should we try to buy buildings off-campus, could that be cheaper, maybe it’s not worth it to repair certain buildings? Those are the type of questions that need to be asked.”